199601024340 (396692-T)

Dear Esteemed Shareholders,

The Management Discussion and Analysis (“MD&A”) is intended to provide shareholders with operational and financial highlights of CCK Consolidated Holdings Berhad (“CCK” or “the Group”) for the financial year ended 31 December 2025 (“FY2025”).

The MD&A should be read together with the audited financial statements of the Group and Company as set out in this Annual Report.

CCK’s business comprises four (4) segments, namely retail, poultry, prawn, and food service. Business operations are carried out primarily in Sarawak, Sabah, and Indonesia (Jakarta, Pontianak, and Tarakan). The Group employs 3,072 employees across all business segments.

The Group’s mainstay and core business is the retail segment, which operates three distinct store formats comprising retail stores, supermarkets, and wholesale outlets. Since the opening of its first retail store in Sibu in 1970, CCK’s network has expanded to seventy-nine (79) touchpoints comprising retail stores, supermarkets, and wholesale outlets across East Malaysia (Sarawak and Sabah). Retail stores operate under the CCK Fresh Mart brand, while supermarkets operate under the CCKLocal brand.

CCK Fresh Mart retail stores cater to both businesses and households, offering a curated range of stock keeping units (“SKUs”) tailored to specific locations and customer demographics. These stores are typically smaller-format outlets located in both urban and rural areas.

CCKLocal supermarkets generally occupy a larger footprint and offer households a wider range of SKUs, including local and imported food items as well as general household products.

CCK’s wholesale outlets primarily serve bulk purchasers and business customers, including food service operators and small retailers, providing a reliable channel for larger-volume purchases. These outlets play a key role in supporting the Group’s distribution reach and complement its retail operations by catering to a broader customer base with differing purchasing needs.

Underpinning these three store formats is CCK’s extensive and fully integrated supply chain, which includes feedmill operations, layer and broiler farming, poultry processing, prawn farming and processing, and the manufacturing of house-brand food products. The Group also procures its own imported frozen goods as well as fresh produce, including fruits and vegetables, ensuring consistency in quality and supply. This is further supported by the Group’s logistics infrastructure, comprising coldrooms as well as a fleet of cold and ambient trucks, enabling efficient storage, handling, and distribution of products across its network.

The Group’s retail network benefits from vertical integration with its poultry segment. On a blended basis, fresh dressed chicken and chicken parts account for approximately 15% of products sold at CCK Fresh Mart outlets, while the remaining 85% comprises house-brand and third-party frozen products, seafood, fresh fruits, and vegetables.

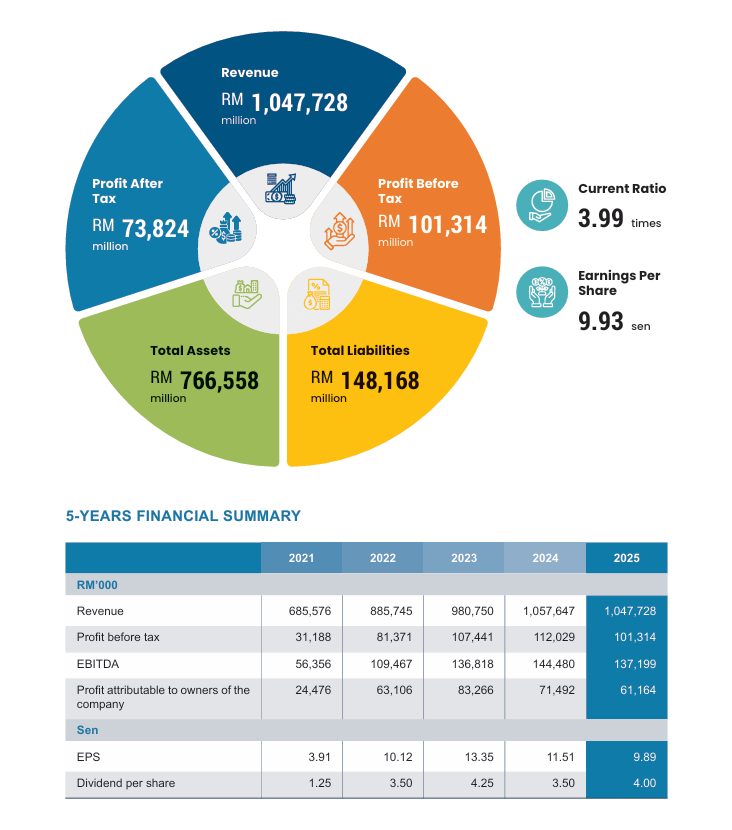

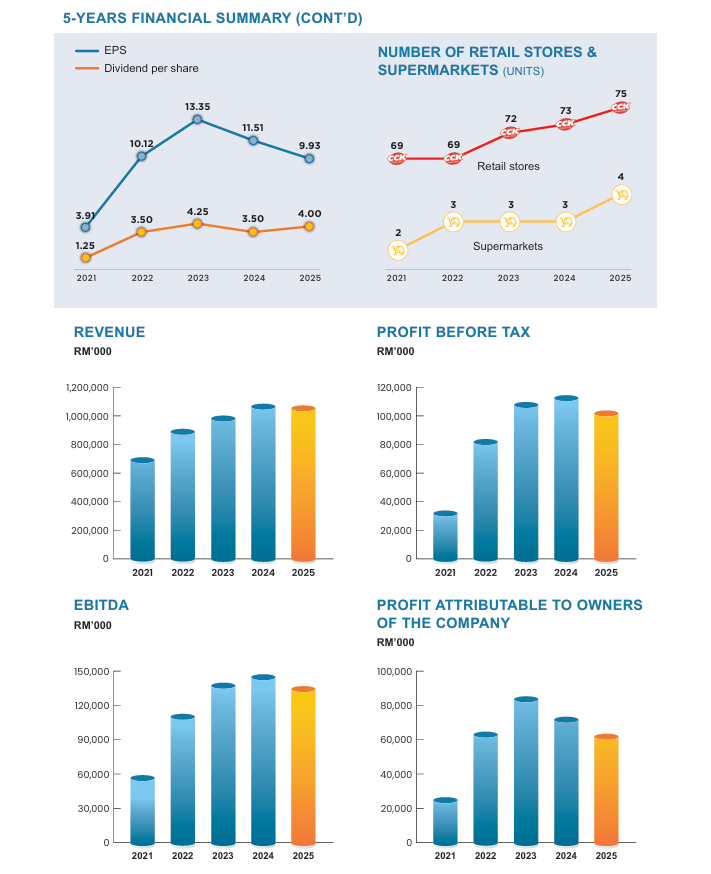

Group revenue for FY2025 was recorded at RM1,047.7 million, compared to RM1,057.6 million in FY2024. This performance was driven by higher contributions from the retail and prawn segments, offset by softer contributions from the poultry and food service segments.

During FY2025, the Group opened two (2) new CCK Fresh Mart retail stores in Benoni, Sabah and Lawas, Sarawak, and closed one (1) outlet in Bintangor, Sarawak. In addition, one (1) CCKLocal supermarket was opened in Bintulu, Sarawak. This brought the Group’s retail network to sixty-nine (69) CCK Fresh Mart stores, four (4) CCKLocal supermarkets, and six (6) wholesale stores, totalling seventy-nine (79) touchpoints.

The retail segment generated RM825.6 million in revenue, compared to RM819.9 million in FY2024. This increase was primarily driven by contributions from the established retail network supported by resilient customer demand. Demand for in-house manufactured processed products in Indonesia also remained strong.

The Group’s Indonesian manufacturing operations were able to support this demand, underpinned by additional production capacity commissioned previously. Revenue from these operations (Pontianak and Jakarta) grew by 5.2% to RM223.6 million, representing 21.34% of total Group revenue.

The poultry segment recorded revenue of RM342.6 million, representing a decline of 8.6% compared to FY2024. This was mainly due to lower sales volumes from both institutional clients and the Group’s own retail network (intersegment sales).

The prawn segment’s revenue increased by 2.5% to RM93.6 million, supported by stronger sales in the Indonesian domestic market. Export volumes remained stable, with increased shipments to Korea, Singapore, Hong Kong, and China offsetting moderation in Japan and Taiwan.

The food service segment recorded revenue of RM16.5 million, compared to RM20.8 million in FY2024, reflecting lower sales volumes and reduced demand from government schools in Sarawak under existing supply contracts.

Group profit before tax (“PBT”) for FY2025 stood at RM101.3 million, compared to RM112.0 million in FY2024. The decline was mainly attributable to lower contributions from the poultry and retail segments, partially offset by improved profitability in the prawn segment, while the food service segment remained relatively stable. Gross profit margin remained stable at 21.30%, compared to 21.36% in FY2024.

The retail segment recorded PBT of RM68.2 million, a decrease of 15.6% from RM80.8 million in FY2024. Profitability was impacted by lower sales volumes from the domestic retail network and strategic pricing adjustments aimed at enhancing competitiveness. Contributions from Indonesian operations helped mitigate this impact.

The poultry segment reported PBT of RM20.3 million, down 17.4% from RM24.6 million in FY2024, primarily due to lower government subsidies related to price ceilings for broilers and table eggs.

The prawn segment recorded PBT of RM11.3 million, an increase of 24.9% from RM9.1 million in FY2024, driven by higher revenue and improved sales mix.

The food service segment reported PBT of RM1.4 million, largely unchanged from RM1.5 million in FY2024.

Share of results from associate company Gold Coin (Sarawak) Sdn Bhd increased to RM5.2 million from RM5.0 million in FY2024.

Operating and administrative expenses increased due to the expansion of the Group’s retail network in Sabah and Sarawak, as well as ongoing capacity expansions in Indonesia under PT Adilmart.

Finance costs for FY2025 amounted to RM3.0 million. Total borrowings stood at RM57.2 million against shareholders’ funds of RM555.1 million as at end-December 2025, translating to a gearing ratio of 0.10 times.

The Group maintained a net cash position, with deposits and cash balances amounting to RM166.2 million.

Property, plant, and equipment increased to RM257.8 million from RM232.2 million a year earlier. Capital expenditure during FY2025 included new retail outlets, upgrades to poultry farming infrastructure in Sabah and Sarawak, and ongoing construction of PT Adilmart’s food processing facility in Boyolali, Indonesia. These investments were funded through a combination of internally generated funds and bank borrowings.

In FY2025, the Group expanded its retail network with:

• Two (2) CCK Fresh Mart retail stores in Benoni, Sabah and Lawas, Sarawak

• One (1) CCKLocal supermarket in Bintulu, Sarawak

One (1) CCK Fresh Mart retail store in Bintangor, Sarawak was closed during the year. In December 2024, the Group completed the disposal of a 37.7% stake in PT Adilmart to Astrantia. This strategic partnership is intended to support the next phase of growth by enhancing operational capabilities, expanding production capacity, and opening new sales channels, while strengthening brand development efforts in Indonesia.

In line with this, the Group is in the process of commissioning a third manufacturing facility in Boyolali, Central Java, with construction progressing throughout FY2025 and expected to come on stream in FY2026.

CCK adopts a policy of dealing with creditworthy customers based on careful evaluation of each customer’s financial standing and credit history. This mitigates the risk of financial loss arising from potential defaults. The Group also maintains a credit monitoring process to regularly track customer payment behaviour.

The Group imports frozen products for its retail network, with purchases denominated in US dollars. As such, the Group is exposed to foreign currency fluctuation risk. Adverse movements in the MYR/USD exchange rate may impact profitability. In addition, currency fluctuations may affect feed costs for the poultry segment.

The Group maintains adequate cash and banking facilities to ensure sufficient liquidity to meet its obligations as they fall due. Exposure to liquidity risk arises primarily from trade payables, other payables, and bank borrowings, including bankers’ acceptances and revolving credit facilities.

The Group’s retail operations face increasing competition from existing and new market participants offering similar products, particularly on pricing. To mitigate this, the Group continues to enhance its competitive positioning through pricing strategies, leveraging its vertically integrated supply chain, and expanding its retail network to drive economies of scale, alongside ongoing improvements in business models and overall customer experience.

Biosecurity and disease risk remain key concerns for the Group’s poultry operations. A disease outbreak at any farm could have a significant financial impact. Accordingly, strict monitoring and biosecurity protocols are implemented across all operations, with continuous enhancements to safeguard livestock health.

CCK has an internal dividend policy of paying up to 30% of the profit after taxation and minority interests whilst taking into consideration the level of available funds, the amount of retained earnings, capital expenditure commitments and other investment planning requirements.

The Board is pleased to announce a final single-tier dividend of 4.0 sen per share for the financial year ended 31 December 2025.

Operating in an increasingly dynamic retail environment, CCK remains focused on delivering essential consumer staples through its extensive urban and rural network across East Malaysia. The Group continues to cater to a diverse customer base, supported by a wide range of offerings including poultry, fresh produce, seafood, and both house brand and third-party frozen products.

Looking ahead to 2026, the Group expects its established retail network to continue delivering stable performance, underpinned by resilient demand for essential food products. Expansion of the retail network will be pursued in a disciplined and measured manner, with a focus on optimising store performance, enhancing operational efficiency, and strengthening market presence across key locations in Sarawak and Sabah.

The Group’s vertically integrated supply chain remains a key competitive advantage, enabling greater control over costs, quality, and product availability. This positions the Group to respond effectively to evolving market conditions while maintaining operational resilience.

That said, the Group remains mindful of external headwinds, including inflationary pressures, currency volatility, and ongoing geopolitical developments. Heightened tensions in the Middle East have contributed to volatility in energy prices, which in turn may lead to higher transportation and shipping costs, as well as increases in agricultural commodity prices. This could result in elevated feed costs for the poultry segment and broader cost pressures across the supply chain. Accordingly, the Group continues to prioritise cost optimisation, operational efficiency, and prudent pricing strategies to safeguard margins while maintaining competitiveness.

In Indonesia, the Group continues to strengthen its Rewarding excellence manufacturing capabilities under PT Adilmart. The ongoing development of a new food processing facility in Boyolali, Central Java, is expected to come on stream in 2026 and will further enhance production capacity, improve operational efficiencies, and support the expansion of new sales channels across the region. This facility is expected to complement the Group’s existing operations in Jakarta and Pontianak, strengthening its ability to meet growing demand for in-house processed products. The Group’s strategic partnership with Astrantia is also expected to support this next phase of expansion.

The Group will continue to focus on disciplined execution, cost management, and operational efficiency while advancing its growth initiatives. The Board remains cautiously optimistic regarding the Group’s performance in the coming financial year.

I would like to extend my sincere appreciation to the Board of Directors, Management team, and all employees of CCK for their dedication, perseverance, and unwavering commitment. Your collective efforts have been instrumental in driving the Group’s continued success and enabling us to navigate an evolving retail landscape with resilience and confidence.

I also extend my appreciation to our valued shareholders, business partners, and stakeholders for your continued support, trust, and collaboration. Your confidence in us drives our commitment to continuously improve, innovate, and deliver sustainable value.

As we move forward, we remain focused on building on our achievements and strengthening our position. We are confident in our ability to execute our strategies and deliver long-term value.